Let me be real with you. I’ve helped dozens of home buyers navigate the Connecticut market, and almost every single one of them has said the same thing: “I had no idea there were this many costs.” They see the listing price. They do the math on the mortgage. And they think, Okay, I’m ready. But then the real numbers show up. The closing costs. The inspections. The attorney fees. The moving truck. The “oh wait, I need a lawnmower now?” moment. So I sat down and mapped out every single dollar you’ll likely spend when buying a new home in Connecticut, from the first pre-approval call to the moment you turn the key in your front door.

Here’s the honest breakdown.

a) The Down Payment: How Much Do You Really Need to Hand Over?

Most people assume you need 20% down. That’s the old-school rule. But in 2026? You’ve got options.

Connecticut’s median home price is hovering around $449,100 right now. Here’s what your down payment could look like depending on your loan type:

- 3% down (conventional or FHA for first-timers): ~$13,473

- 5% down: ~$22,455

- 10% down: ~$44,910

- 20% down: ~$89,820

Here’s the thing I always tell my clients: don’t drain your savings to hit 20%. If you qualify for CHFA or FHA programs, you can put down way less and keep cash in your pocket for repairs, furniture, and that inevitable “welcome to homeownership” plumbing bill.

Also, if you’re wondering, should I buy a house in Connecticut with less than 20% down, yes, absolutely. Just budget for PMI (private mortgage insurance), which runs about $185 to $626 a month depending on your loan size.

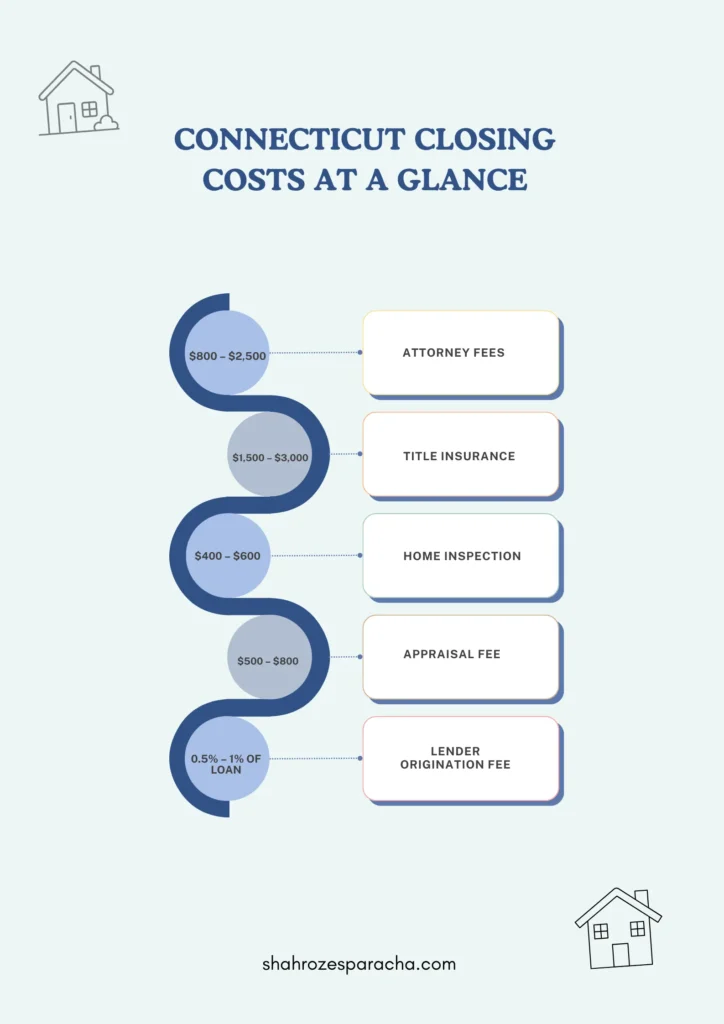

b) Closing Costs: The Sneaky $10k+ You Forgot About

This is the part that trips up most home buyers. You see the price tag, you save for the down payment, and then, surprise: Here comes another stack of fees.

In Connecticut, closing costs typically run 2% to 5% of the purchase price. On that $449,100 home, that’s $8,982 to $22,455.

Why so much? Because Connecticut requires attorney representation for real estate transactions. And attorneys aren’t cheap, but they will save your neck if something goes sideways.

Pro tip from someone who’s seen too many buyers panic at the closing table: ask for a seller concession. You can negotiate 1% to 3% of the sale price back from the seller to cover some of these costs. It works more often than you’d think.

c) The Monthly Burn: What It Actually Costs to Live in Your Connecticut Home

You bought the house. Congratulations! Now here’s what leaves your bank account every single month:

- Mortgage (principal + interest): ~$2,227

- Property taxes: ~$617 (CT has the 7th highest property tax rate in the US)

- Homeowners insurance: ~$135

- Maintenance reserve: ~$353 (and honestly, budget 2% of home value; that’s more realistic)

- Utilities: ~$463 (hello, Connecticut winters)

Total monthly: About $3,795

I know. That number stings a little. But here’s the mindset shift that helped my past clients: think of this as the cost of living in Connecticut with stability, equity, and a place that’s actually yours. Rent in Fairfield County for a comparable property? You’re looking at $3,000+ anyway, and that money vanishes forever.

d) Hidden Costs Nobody Warns You About (Until Now)

Credit: realtor.com

Alright, let me pull back the curtain on expenses that don’t show up in your loan estimate but will show up in your first year:

- i. The “I just bought a house” tax: Moving truck ($1,250 – $4,890), new locks, curtains, maybe a fridge if the seller took theirs. I spent $800 on curtain rods alone my first month. True story.

- ii. Immediate repairs: The inspection found it; you negotiated a credit, but you still have to do the work. Budget $2,000 – $5,000 for the first 90 days.

- iii. HOA fees: If you’re buying in a condo or planned community. The national average is ~$250/month. In Stamford or downtown Hartford? Could be double that.

- iv. PMI (if you put down less than 20%): That’s $185 to $626 extra per month until you hit 20% equity.

- v. Your emergency fund: I tell every buyer: keep at least 3 months of mortgage payments in savings after closing. Because the water heater will wait until the worst possible moment to die.

e) Where in Connecticut Should You Buy? The Affordability Map

If you’re asking yourself what is the best place in Connecticut to buy a house, the answer depends on your budget and lifestyle. But here are some real numbers:

More affordable cities (where your dollar goes further)

- East Hartford: Median home price around $260k. Seriously. One of the cheapest places in Connecticut to buy a home.

- Hartford: $321k median. Urban, walkable, huge inventory.

- New Britain: Under $300k. Up-and-coming.

- Windham: One of the most affordable places to live in the state.

Mid-range cities (good balance of price and lifestyle)

- Manchester: $350k – $400k. Great schools, strong community.

- South Windsor: $400k+. Growing fast.

- Vernon: $320k+. Solid value.

Premium markets (higher prices, higher lifestyle)

- Stamford: $600k+. If you’re researching buying a house in Stamford, Connecticut, expect NYC-adjacent pricing.

- Glastonbury: $500k+. Top schools, top taxes.

- West Hartford: $450k+. Blue-ribbon schools, charming Blue Back Square.

And if you’re the adventurous type wondering if it’s worth buying a house to renovate in Connecticut, yes, in cities like New London, Bridgeport, or Waterbury, you can find fixer-uppers under $200k and build instant equity. Just budget 20% extra for surprises.

The Bottom Line

Wrapping up, get pre-approved first. Know your number. Then compare listing prices against median household income in each town. That’s how you find what’s actually realistic. Look, buying a new home in Connecticut isn’t cheap. I won’t lie to you. But the buyers who succeed do three things: they budget for closing costs, they never skip the inspection, and they work with a real estate pro who has their back.

Whether you’re eyeing East Hartford for affordability or dreaming of that colonial in Glastonbury, let’s run the numbers. No surprises. Just a clear path to your new front door.

FAQ’s

Buying a new home in Connecticut? Let’s answer some of your queries here!

What is the 3-3-3 rule for home buying?

Spend no more than 30% of your gross income on your mortgage, keep 3 months of payments in an emergency fund, and plan to own the home for at least 3 years to ensure equity growth.

How much do you have to make a year to qualify for a $400,000 house?

Generally, you need a gross annual income between $120,000 and $135,000. This ensures your monthly payment stays within the recommended 28% debt-to-income ratio.

What credit score do I need to buy a home in Connecticut?

You can qualify for an FHA loan with a 580 score, while conventional loans usually require at least 620. Aim for 740+ to secure the lowest possible interest rates.

Who pays the realtor fees in Connecticut?

While buyers now negotiate fees directly with their agent, we frequently negotiate “seller concessions” to have the seller cover these costs at closing, keeping your out-of-pocket expenses low.

Is it cheaper to build or buy an existing home in CT?

Buying an existing home is significantly cheaper. New construction often exceeds $200 per square foot, excluding the cost of land and utility hookups, whereas existing homes offer much better value.